Lavallee v. Med-1 Solutions, LLC from the U.S. Court of Appeals for the Seventh Circuit examines whether an email from a debt collector was an “initial communication” and if it was, whether a clickable hyperlink serves as a proper means of providing the validation notice mandated by section 1692g(a) of the federal Fair Debt Collection Practices Act. These disclosures, sometimes called the “validation notice,” can be contained in what the FDCPA refers to as the “initial communication” or provided “in writing” within five days of the initial communication.

Lavallee v. Med-1 Solutions, LLC from the U.S. Court of Appeals for the Seventh Circuit examines whether an email from a debt collector was an “initial communication” and if it was, whether a clickable hyperlink serves as a proper means of providing the validation notice mandated by section 1692g(a) of the federal Fair Debt Collection Practices Act. These disclosures, sometimes called the “validation notice,” can be contained in what the FDCPA refers to as the “initial communication” or provided “in writing” within five days of the initial communication.

While the debt collector was found to have violated the FDCPA, the decision offers at least a construct for providing an email validation notice that could pass muster before this court. And perhaps more important, it adopts a restrictive interpretation of what constitutes a “communication” under the FDCPA.

Lavallee incurred several debts to a hospital for medical services. In November 2015, the hospital called her concerning other debts and during that discussion, she learned that two additional debts had been assigned by the hospital to a debt collector, Med-1 Solutions, LLC. Lavallee called Med-1 concerning the additional debts later the same day.

Lavallee sued alleging that the call she placed to Med-1 was her “initial communication” concerning the two debts and that Med-1 failed to provide the 1692g(a) disclosures during the telephone call or in writing within five days.

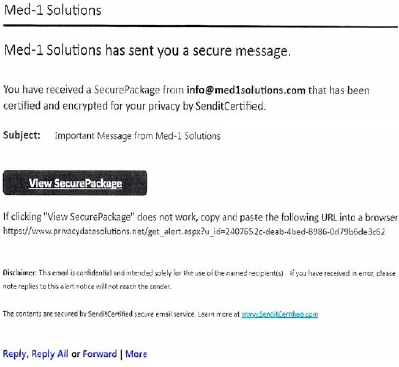

Med-1 saw it differently — Lavallee’s November 2015 telephone call was not the initial communication concerning her debts. Instead, it was two emails Med-1 had sent Lavallee, one for each debt, in March and April 2015. And both emails contained the 1692g(a) disclosures. The emails, similar in form, came from “info@med1solutions.com” and were sent to the email address Lavallee provided to the hospital. The emails stated “Med-1 Solutions has sent you a secure message” and contained a hyperlink embedded in the text “View SecurePackage.” Clicking on the link would take the recipient to the validation notice containing the information and disclosures required by 1692g(a). The emails didn’t say much else as can be seen from the reproduction contained in the court’s opinion:

The Court of Appeals held that the two emails were not communications as defined by the FDCPA, and so could not be “initial communications” and, even if they were, did not properly provide the validation notice.

What went wrong for the collector in this court’s view is that while an email may be commonly understood as a “communication,” what the FDCPA considers as a “communication” is quite different.

FDCPA “Communications”

Emails can be “communications” within the meaning of the FDCPA. All it takes is for the email to “convey[] … information regarding a debt directly or indirectly.” And there is little doubt such an email would qualify because the FDCPA includes “any medium” as the means of conveying the information.

Here, the collector’s emails, according to the decision, did not qualify as an FDCPA communication because “the emails say nothing at all about a debt.” The emails, after all, do not mention a debt, a debt collector or any collection activity. But there are many who would say the FDCPA’s definition of communication should be read broadly and by its very definition would construe the hyperlink as meeting the test of “conveying … information regarding a debt . . . indirectly.” A person clicking on the hyperlink would receive information concerning the debt, such as the amount and the name of the creditor to whom the debt is owed, as well as a disclosure that the company was acting as a debt collector, among other things. The opinion does little to explore this issue.

Hyperlink Delivery of Validation Notice

The opinion also disapproved of the use of a hyperlink to deliver the validation notice, calling it “at best . . . a digital pathway to access the required information.” It analogized the hyperlink delivery to a printed letter that simply contained the location of where the disclosure could be obtained.

The Consumer Financial Protection Bureau recently proposed rules that would also permit the use of “hyperlinks” to deliver the validation notice, “if, among other things, the debt collector or a creditor first provided the consumer with notice and an opportunity to opt out.” One former federal consumer protection regulator criticized the use of hyperlinks as a security risk.

Of course, had the validation notice here been provided in the emails, the decision would probably have turned out much better for the collector on both issues. Section 1692g(a) allows for the validation notice to be “contained in the initial communication.” And since a communication can be conveyed through “any medium,” the validation notice can be provided in an initial communication made by telephone and, by extension, in a similar email, text message or, in a printed letter. On this point, the CFPB filed an amicus brief with the Court of Appeals which framed the issue as “whether [the collector] complied with the FDCPA’s requirement that a debt collector ‘send the consumer a written notice containing’ statutorily required information about the debt.” In framing the issue this way, it is possible that the CFPB did not see Med-1’s hyperlink as satisfying section 1692g(a)’s requirement that the disclosure “is contained in the initial communication.” Unfortunately, the brief does not squarely address this issue.

Lavallee’s Implications

Don’t expect Lavallee to curtail email communications between debt collectors and consumers. Consumer use of emails has steadily grown and, according to one report, an estimated 117.7 billion emails will be sent and received by consumers worldwide per day in 2019. That number compares favorably to the projected 128.8 billion daily emails sent and received by businesses this year.

But what the decision does demonstrate is that emails are interpreted under the FDCPA the same as other means of communication. This is not the case in some states, which impose separate regulations on the use of electronic communications in debt collection.

Join me for my webinar Emails and Hyperlink Delivery of FDCPA Disclosures after Lavallee exploring the landscape for the use of electronic communications in debt collection. In addition to Lavallee and the FDCPA, the webinar will examine state regulation of electronic communications in debt collection, the CFPB’s proposed rules for electronic communications in debt collection and the use of the E-Sign Act. The webinar qualifies for 1.5 RMAI Certification Credits. To view an instant replay of the webinar, register here.