On April 21, the U.S. Court of Appeals for the Eleventh Circuit issued a decision holding that the transmittal of consumer information to a letter vendor constitutes a communication with an unauthorized third party in connection with the collection of a debt in violation of 15 U.S.C. § 1692c(b).

Posts tagged as “Debt Collection”

The U.S. Court of Appeals for the Third Circuit recently affirmed the dismissal of a class action complaint alleging that a collection letter’s itemization of a debt as including “$0.00” in interest and fees — when the debt could not accrue interest or fees — violated the federal Fair Debt Collection Practices Act.

The U.S. Court of Appeals for the Eighth Circuit recently affirmed a trial court’s dismissal of the plaintiffs' claims in consolidated cases brought under the federal Fair Debt Collection Practices Act against a debt collector law firm, after the debt collector law firm failed to meet evidentiary burdens in various collection lawsuits.

On April 7, the Consumer Financial Protection Bureau (CFPB) issued a Proposed Rule that would postpone the effective date of the Debt Collection Final Rules, Part 1 and Part 2, by 60 days, from Nov. 30, 2021, to Jan. 29, 2022.

The U.S. Court of Appeals for the Ninth Circuit recently reversed a trial court’s dismissal of allegations that the defendant violated the federal Fair Debt Collection Practices Act (FDCPA) by sending a collection letter threatening litigation over a time-barred or "out-of-statute" debt and filing a lawsuit seeking to collect the debt.

The U.S. Court of Appeals for the Third Circuit recently held that a debt collector did not violate the federal Fair Debt Collection Practices Act (FDCPA) when it sent a consumer a collection letter inviting her to “eliminate further collection action” by calling the company, when in fact only written communication could legally stop collection activity.

The U.S. Court of Appeals for the Seventh Circuit recently affirmed a trial court’s judgment that an insurer had no duty to defend a debt collector in an action brought by a consumer asserting claims under the federal Fair Debt Collection Practices Act (FDCPA) and the federal Telephone Consumer Protection Act (TCPA), as well as common law claims of defamation and invasion of privacy.

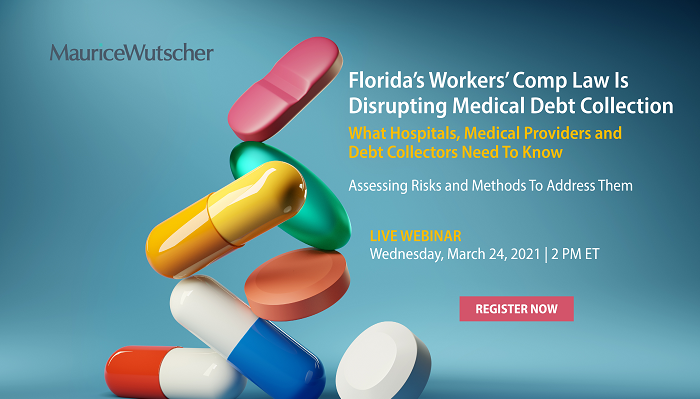

The State of Florida, like many states, maintains a robust workers’ compensation statute geared toward insulating employees injured on the job from associated medical services. Now, lawsuits continue to be filed against debt collectors, hospitals and other medical providers alleging that under a novel interpretation of Florida’s workers’ compensation law, it is unlawful to attempt to collect medical debt arising from work-related injuries directly from consumers.

The U.S. Court of Appeals for the Fifth Circuit recently affirmed the dismissal of a debtor’s claims against a debt collector alleging that a telephone call placed to his sister constituted an improper third-party communication in connection with the collection of a debt, in violation of the federal Fair Debt Collection Practices Act (FDCPA).

The Florida Supreme Court recently resolved a split in Florida law on the issue of attorney’s fees in favor of consumers, holding that debtors who prevail when a creditor sues under an account stated cause of action instead of for breach of the underlying credit card agreement are entitled to recover attorney’s fees under the so-called “reciprocity provision” of subsection 57.105(7), Florida Statutes.

The U.S. Court of Appeals for the Seventh Circuit recently affirmed the dismissal of a consumer’s claims under the federal Fair Debt Collection Practices Act (FDCPA) for failing to sufficiently allege a concrete injury to confer standing under Article III.

The U.S. Court of Appeals for the Seventh Circuit recently vacated a trial court’s judgment of dismissal and remanded with instructions to hold an evidentiary hearing limited to the issue of whether the trial court had subject-matter jurisdiction over a plaintiff’s claim that a dunning letter violated the federal Fair Debt Collection Practices Act because it did not clearly state that interest would accrue on the debt.